How does an obscure factor like hiring practices impact firm valuation? That was the question posed by Deutsche Bank’s quant strategy group in a 2015 whitepaper titled, “Macro and Micro Jobenomics.” The report concluded that online job postings could be used to predict U.S. macroeconomic statistics and equity market returns. This piqued my interest – I wondered whether a similar process could be used for valuing A-share companies in China.

I began by examining self-reported employee headcounts from listed companies.

Firm-level data from DataYes shows that year-on-year revenue growth correlates positively with headcount. The histogram on the left shows correlation coefficients for the 1600 A-share firms with 10 years of historical data. The chart on the right shows that the correlation between headcount and revenue growth varies by sector.

Moving on to the main course, the online hiring data set I used tracks a daily average of 300,000 job postings and covers 819 A-share firms. Each observation includes a job title, location, firm name, education and experience, and pay range.

To facilitate cross-company comparisons, I calculated a “hiring ratio” that divides each firm’s total number of unique job postings by employee headcount. I then tested this factor by comparing the private and state-owned sectors.

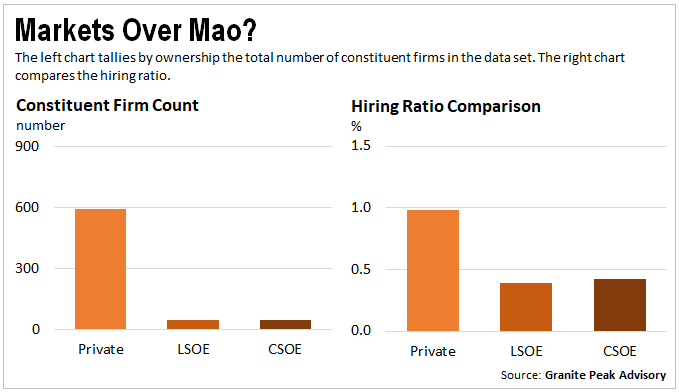

Unsurprisingly, the private sector is much more active on the job market than China’s state-owned-enterprises. In fact, private firms outnumber SOEs in the data set by a factor of six, and their hiring ratio is more than double that of the SOEs.

Insufficient history on Chinese hiring data precludes precisely replicating the back-test methodology of the original whitepaper. As a proxy, I examined the cross-sectional relationship between hiring ratio and firm valuations, which approximate the expectations of future profits from management and investors, respectively.

Controlling for sector, I found that the hiring ratio correlated positively with firm valuation. Obviously, hiring ratio isn’t the sole determinant of firm valuations in China. If it were, most of my banker friends would be out of a job. However, the results of a simple regression results appear predictive enough to warrant consideration.

Of course, much more interesting than the model itself are the outliers – firms with a high hiring ratio and low valuation. The absence of evidence is not evidence of absence, so we will therefore consider only the firms with anonymously high hiring ratios.

As an exercise, I sorted the 1,000 listed companies with highest market capitalization in China by their residual valuation – that is, the underestimation of price-to-sales ratio relative to hiring ratio. In other words, these are the firms that could be considered under-valued if all else were equal.

These findings leave two questions for further research. First, does diversity of the job postings matter? For example, do investors reward firms for hiring across the whole organization rather than just growing the sales team? Second, does average new hire wages impact valuations? That is, do investors reward firms for winning higher-priced talent, under the assumption that they will improve the bottom line?